What does the refreshed HSBC Premier World Elite Mastercard have to offer you?

Links on Head for Points may support the site by paying a commission. See here for all partner links.

This article is an advertisement feature for HSBC Premier

This week sees the relaunch of the HSBC Premier World Elite Mastercard credit card.

This is a very interesting product for the UK miles and points collector. You can transfer the points you earn to more airlines than American Express Membership Rewards offers and the card comes with a big sign-up bonus.

You need to have a HSBC Premier Bank Account to sign-up, so the card isn’t available to everyone.

You can find out more about the HSBC Premier World Elite Mastercard here. Full details of how to apply for HSBC Premier are here.

About the HSBC Premier World Elite card

£290 annual fee, card only available to HSBC Premier Bank Account holders

Representative example:

100.2% APR representative (variable) and 29.9% p.a. (variable) for purchases, based on the annual fee of £290 and an assumed credit limit of £1,200

Credit is subject to status

The HSBC Premier World Elite Mastercard is issued by HSBC Bank UK

What is the HSBC Premier World Elite sign-up bonus?

The sign-up bonus is impressive.

You will receive 40,000 HSBC Reward points, which convert into 20,000 Avios or other airline miles or hotel points, if you spend £2,000 within your first three months. Note that it can take up to 60 days after the three months are over for your bonus to arrive.

What do you earn per £1 spent on the card?

HSBC has just increased the earning rate on the HSBC Premier World Elite Mastercard.

The card gives 3 HSBC points for every £1 spent in the UK and 4 points for every £1 spent abroad. Each point is worth 0.5 airline miles or hotel points.

This means that you earn 1.5 airline miles per £1 for UK spend and 2 miles per £1 for foreign spend, an excellent earn rate!

You can transfer your HSBC points into the following airline schemes:

- Asia Miles

- British Airways Executive Club

- Emirates Skywards

- Etihad Guest

- EVA Air Infinity MileageLands

- Finnair Plus

- Flying Blue (Air France KLM)

- Qantas Frequent Flyer

- Qatar Airways Privilege Club

- Singapore Airlines KrisFlyer

- TAP Miles&Go

There are also two hotel partners:

- IHG One Rewards

- Wyndham Rewards

Transfers to most, possibly all, partners are instantaneous which is very rare in the UK market. This is valuable if you see a reward flight available and want to lock it in before it disappears.

Your points will expire after three years, irrespective of whether you are still earning, so don’t forget to redeem them!

What are the alternatives if you don’t want travel points?

The main alternative to redeeming your HSBC Premier credit card points for airline miles or hotel points is to redeem for shopping vouchers.

1,500 HSBC points gets you £5 of vouchers. Retailers include Amazon, M&S, John Lewis & Waitrose, Airbnb and lastminute.com.

The other ways to spend your points are ordering wine from a limited selection at Laithwaites or having trees planted in your name.

Since the same 1,500 HSBC points would get you 750 airline miles, we suspect that most HfP readers will choose that over a £5 shopping voucher, even though that’s an effective 1% cashback if vouchers are chosen. The choice is there, however.

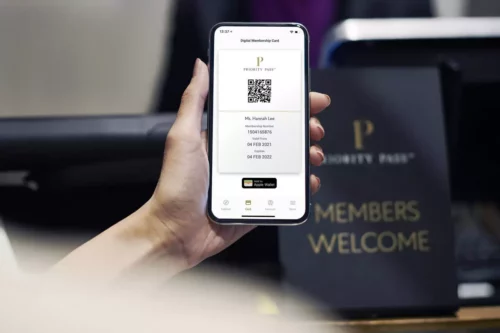

There is an airport lounge benefit

You will receive free, unlimited, access via the Priority Pass scheme to over 1,300 airport lounges.

No free guests are allowed into the lounges. However, you can get a supplementary card for your HSBC Premier World Elite Mastercard for a £60 annual fee and the holder can access lounges with it.

Additional guests, including children, can get access for a £24 guest fee which is charged directly to your HSBC Premier World Elite Mastercard.

The Priority Pass issued by HSBC is better than the American Express-issued version because it includes the restaurant benefit. Many airport restaurants give an £18 food and drink credit to Priority Pass holders, but American Express opts out of this benefit. This article shows you the UK airport restaurants which will give you an £18 credit each time you visit.

Airport fast track is now available too

A new benefit added to the HSBC Premier World Elite Mastercard this week is airport fast track security.

This is available at participating airports worldwide via Mastercard Travel Experiences.

The benefit is only available for the cardholder and any supplementary cardholders.

Other card benefits include ….

Your HSBC Premier World Elite Mastercard comes with other travel benefits including

- Up to 10 per cent discount on selected hotels booked through Expedia

- Up to 14% per cent discount on selected hotels booked through Agoda

Other HSBC Premier benefits include ….

HSBC Premier includes other travel benefits as part of the base package. There is no requirement to take out a credit card to benefit from these.

The key benefit is full travel insurance. You must be aged under 70 years to be covered and terms and conditions apply. The eligibility page for HSBC Premier Bank Accounts has more information.

You also benefit from:

- Access to further offers and discounts through Home&Away – this currently includes a 15% discount on Heathrow Express tickets for HSBC Premier Bank Account holders

- Access to experiences and events in cities globally with Mastercard Priceless

As we always say, travel reward credit cards generally have high interest rates and are not suitable for anyone who does not pay off their full balance each month. If you do not clear your balance, you should look for a non-rewards credit card with a low interest rate.

There are two HSBC Premier credit cards, both of which earn points which can be converted to airline miles and hotel points. This article is looking at the refreshed HSBC Premier World Elite Mastercard, but you can find out more about the No Annual Fee version in our HSBC Premier Mastercard review here.

What are the requirements to apply for the card?

The HSBC Premier World Elite Mastercard differs from other travel rewards cards you may have because the card can only be obtained if you have a HSBC Premier Bank Account.

The criteria for HSBC Premier changed at the beginning of September and are now more straightforward. See here and scroll down.

There are three ways of meeting the criteria:

- have an individual annual income of at least £100,000, and pay your annual income into your HSBC Premier Bank Account

- have savings or investments of at least £100,000 with HSBC in the UK

- hold and qualify for HSBC Premier in another country or region

You also have to meet standard criteria over your age, where you live, proof of identity and pass a credit check. The ‘savings or investments’ criteria excludes M&S, first direct and HSBC Expat. For joint accounts, at least one party much have an individual income of at least £100,000.

Conclusion

The new HSBC Premier World Elite Mastercard has a lot to offer:

- a high earning rate of 1.5 airline miles per £1 spent

- a strong sign-up bonus equivalent to 20,000 airline miles

- airport lounge access, including access to Priority Pass airport restaurant credits

- fast track security access with DragonPass

- includes travel insurance via the requirement to hold a HSBC Premier Bank Account

You also get the wider benefits of having your current account with HSBC Premier. Remember there is a requirement to hold the HSBC Premier Bank Account, so if you meet the eligibility criteria it is well worth a look given the benefits.

You can find out more about the HSBC Premier World Elite Mastercard here. Full details of how to apply for HSBC Premier are here.

Disclaimer: Head for Points is a journalistic website. Nothing here should be construed as financial advice, and it is your own responsibility to ensure that any product is right for your circumstances. Recommendations are based primarily on the ability to earn miles and points. The site discusses products offered by lenders but is not a lender itself. Robert Burgess, trading as Head for Points, is regulated and authorised by the Financial Conduct Authority to act as an independent credit broker.

sturgeon

sturgeon  points_worrier

points_worrier  BBbetter

BBbetter  EvilGazebo

EvilGazebo  Swiss Jim

Swiss Jim  Kowalski

Kowalski  memesweeper

memesweeper  Jonathan

Jonathan  JDB

JDB  Magic Mike

Magic Mike  Froggee

Froggee  Freddy

Freddy  Mr zee

Mr zee  Sam

Sam  Steven

Steven  TGLoyalty

TGLoyalty

Comments (118)