Interesting anomalies in Avios flight reward pricing you can exploit

Links on Head for Points may support the site by paying a commission. See here for all partner links.

Some Avios redemptions are ‘disproportionately’ cheap because they fall right on the edge of an Avios pricing band.

If you know how to use this knowledge to your advantage, you make decent savings in Avios and/or taxes on your next long-haul redemption.

How can Avios pricing anomalies make flights cheaper?

Until Aer Lingus rigged the game by forcibly moving it into the higher band, Dublin to Boston was the prime example of this.

At 2,993 miles it used to be a bargain as it fell into the cheaper “sub 3,000 miles” pricing of 75,000 Avios return in Business. Instead of paying 100,000 off-peak or 120,000 peak Avios on a direct BA flight from London, you could make a chunky saving by taking a cheap flight to Dublin to start your journey.

Aer Lingus eventually decided to spoil the fun. It has now decided that Boston is 8 miles further away than it really is, so it now costs 100,000 or 120,000 Avios depending on whether it is a ‘peak’ day. There is no Avios saving compared to flying BA from London, although the substantial £400 tax saving remains.

Back in 2013, spurred on by an article I wrote on the topic, the team at Flyertalk produced some fantastic diagrams to highlight potential pricing anomalies. These make it easy to spot interesting redemptions which might be surprisingly good value.

I have only focused on one example in this article, but if you click here to visit Flyertalk you will see them for virtually all oneworld airline hubs.

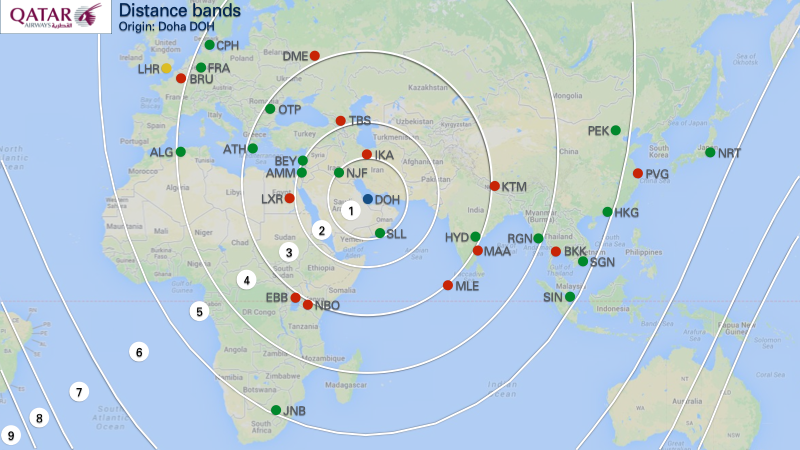

This example chart shows Avios pricing bands for Qatar Airways, radiating out from Doha (click to enlarge):

The numbers refer to the nine Avios pricing bands for flights on partner airlines (click to enlarge):

Let’s take a look at the Qatar Airways chart in detail. A green dot means that the city is in the lower priced band. A red dot means that the city is in the higher priced band.

An example to Doha

London to Doha, as you can see, is Zone 5.

Flying direct on British Airways, you pay 120,000 Avios return in Club World Business Class on a ‘peak’ day – this prices off the BA reward chart, not the partner chart shown above – plus £502.

Flying direct on Qatar Airways, you pay 124,000 Avios return in Business Class plus £500.

Frankfurt, though, is just in Zone 4. This means you pay only 77,500 Avios return in Business Class from Frankfurt to Doha. Taxes are £479 return.

As you get a return Avios flight on British Airways to Frankfurt for 9,000 Avios plus £35, you can save 33,500 Avios on peak date Business Class redemptions to Doha by connecting in Frankfurt, albeit with an Economy connecting flight.

(A warning – if you book both flights on the same ticket, the taxes figure will jump up because you will need to pay long-haul Air Passenger Duty. If you book both flights on separate tickets, you could be in trouble if you miss your connection. The choice is yours.)

An example to Singapore

You will also see that Singapore is conveniently placed on the edge of Zone 5. This means that, whilst connecting usually means a bad deal when redeeming with Avios, in this case it works out OK.

Frankfurt to Singapore via Doha is 100,750 Avios plus £306 tax (business, one-way).

London to Singapore on BA, non-stop – a VERY tricky seat to find – is 105,000 Avios plus £393 tax one-way on a peak day.

Add in 4,500 Avios + £17.50 for a one-way flight to Frankfurt and the Avios cost is roughly equal. Clearly one of these trips requires three flights and the other is direct, but the £70 tax saving compensates partially – and, of course, you’re flying Qatar Airways in the amazing Qsuite if you choose the right aircraft.

In any event, it has historically been VERY hard to get seats on the direct British Airways Singapore service so you may end up looking for an alternative.

(Whilst we are using Doha as an example here, there is actually an even sweeter spot to Singapore. Frankfurt to Singapore on Cathay Pacific, changing in Hong Kong, is only 114,750 Avios + £113 one way. This is a great deal if you want to minimise taxes and charges.)

There’s more ….

You can spend ages playing with these charts and working out options. Over at Flyertalk you will find them for:

- Aer Lingus ex-Dublin

- American Airlines ex-Los Angeles

- American Airlines ex-New York

- American Airlines ex-Chicago

- American Airlines ex-Dallas

- American Airlines ex-Miami

- Cathay Pacific ex-Hong Kong

- Iberia ex-Madrid

- Malaysia Airlines ex-Kuala Lumpur

…. as well as generic charts from Delhi and Singapore.

Note – and this is very important – that the charts in the Flyertalk article were created before the 2015 Avios devaluation and the 2019 partner airline price rises. All of the Avios pricing examples given in that thread are now wrong and you will need to re-work the numbers. The charts themselves are still accurate, however, as the Avios bandings did not change.

All of the charts can be found in this Flyertalk thread.

PS. If you are not a regular Head for Points visitor, why not sign up for our FREE weekly or daily newsletters? They are full of the latest Avios, airline, hotel and credit card points news and will help you travel better. To join our 70,000 free subscribers, click the button below or visit this page of the site to find out more. Thank you.

How to earn Avios from UK credit cards (July 2025)

As a reminder, there are various ways of earning Avios points from UK credit cards. Many cards also have generous sign-up bonuses!

In February 2022, Barclaycard launched two exciting new Barclaycard Avios Mastercard cards with a bonus of up to 25,000 Avios. You can apply here.

You qualify for the bonus on these cards even if you have a British Airways American Express card:

Barclaycard Avios Plus Mastercard

Get 25,000 Avios for signing up and an upgrade voucher at £10,000 Read our full review

Barclaycard Avios Mastercard

Get 5,000 Avios for signing up and an upgrade voucher at £20,000 Read our full review

There are two official British Airways American Express cards with attractive sign-up bonuses:

British Airways American Express Premium Plus Card

30,000 Avios and the famous annual Companion Voucher voucher Read our full review

British Airways American Express Credit Card

5,000 Avios for signing up and an Economy 2-4-1 voucher for spending £15,000 Read our full review

You can also get generous sign-up bonuses by applying for American Express cards which earn Membership Rewards points. These points convert at 1:1 into Avios.

American Express Preferred Rewards Gold Credit Card

Your best beginner’s card – 20,000 points, FREE for a year & four airport lounge passes Read our full review

The Platinum Card from American Express

50,000 bonus points and great travel benefits – for a large fee Read our full review

Run your own business?

We recommend Capital on Tap for limited companies. You earn points worth 0.8 Avios per £1 on the FREE standard card and 1 Avios per £1 on the Pro card. Capital on Tap cards also have no FX fees.

Capital on Tap Visa

NO annual fee, NO FX fees and points worth 0.8 Avios per £1 Read our full review

Capital on Tap Pro Visa

10,500 points (=10,500 Avios) plus good benefits Read our full review

There is also a British Airways American Express card for small businesses:

British Airways American Express Accelerating Business Card

30,000 Avios sign-up bonus – plus annual bonuses of up to 30,000 Avios Read our full review

There are also generous bonuses on the two American Express Business cards, with the points converting at 1:1 into Avios. These cards are open to sole traders as well as limited companies.

The American Express Business Platinum Card

50,000 points when you sign-up and an annual £200 Amex Travel credit Read our full review

The American Express Business Gold Card

20,000 points sign-up bonus and FREE for a year Read our full review

Click here to read our detailed summary of all UK credit cards which earn Avios. This includes both personal and small business cards.

Maximus

Maximus

Comments (21)