Earn 26,000 miles with a new Virgin Flying Club life insurance deal

Links on Head for Points may support the site by paying a commission. See here for all partner links.

Virgin Flying Club has relaunched its offer with Virgin Money life insurance – and with a slightly higher mileage incentive.

Until 15th January 2020 Virgin Atlantic Flying Club members who take out a life insurance policy from Virgin Money will receive up to 26,000 Flying Club miles.

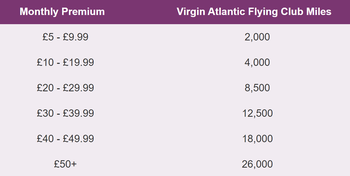

The number of miles you can earn varies by the monthly premium you choose:

This is a little better than it was when the offer last ran. The £40 band now offers 18,000 miles vs 16,000 miles, for example. The £50+ band went up from 25,000 miles to 26,000 miles.

The small print says that the miles will arrive up to 60 days after the sixth consecutive monthly payment. You will therefore be paying £300 to earn 26,000 miles if you pick a £50 per month policy.

It isn’t worth taking out unnecessary insurance purely for the miles. On the other hand, if you are currently paying for cover and can get a similar policy from Virgin Money for a similar price, this could be an easy way of picking up 26,000 miles.

The application website is here.

PS. If you are not a regular Head for Points visitor, why not sign up for our FREE weekly or daily newsletters? They are full of the latest Avios, airline, hotel and credit card points news and will help you travel better. To join our 70,000 free subscribers, click the button below or visit this page of the site to find out more. Thank you.

How to earn Virgin Points from UK credit cards (July 2025)

As a reminder, there are various ways of earning Virgin Points from UK credit cards. Many cards also have generous sign-up bonuses.

You can choose from two official Virgin Atlantic credit cards (apply here, the Reward+ card has a bonus of 18,000 Virgin Points and the free card has a bonus of 3,000 Virgin Points):

Virgin Atlantic Reward+ Mastercard

18,000 bonus points and 1.5 points for every £1 you spend Read our full review

Virgin Atlantic Reward Mastercard

3,000 bonus points, no fee and 1 point for every £1 you spend Read our full review

You can also earn Virgin Points from various American Express cards – and these have sign-up bonuses too.

The American Express Preferred Rewards Gold Credit Card is FREE for a year and comes with 20,000 Membership Rewards points, which convert into 20,000 Virgin Points.

American Express Preferred Rewards Gold Credit Card

Your best beginner’s card – 20,000 points, FREE for a year & four airport lounge passes Read our full review

The Platinum Card from American Express comes with 50,000 Membership Rewards points, which convert into 50,000 Virgin Points.

The Platinum Card from American Express

50,000 bonus points and great travel benefits – for a large fee Read our full review

Small business owners should consider the two American Express Business cards. Points convert at 1:1 into Virgin Points.

The American Express Business Platinum Card

50,000 points when you sign-up and an annual £200 Amex Travel credit Read our full review

The American Express Business Gold Card

20,000 points sign-up bonus and FREE for a year Read our full review

Click here to read our detailed summary of all UK credit cards which earn Virgin Points.

Benilyn

Benilyn  Michael

Michael  memesweeper

memesweeper  marcw

marcw  Matt k

Matt k  Shoestring

Shoestring  David

David  Lev441

Lev441  Nick_C

Nick_C  Freddy

Freddy

Comments (67)