American Express will pay you 0.9p CASH for your Membership Rewards points

Links on Head for Points may support the site by paying a commission. See here for all partner links.

American Express has launched a very interesting offer for holders of The Platinum Card.

If you use your points for statement credit (ie reducing what you owe next month by redeeming points) you would usually receive a pitiful £4.50 per 1,000 points.

This new offer is worth £9 per 1,000 Membership Rewards points. This is surprisingly good.

What are Membership Rewards points worth?

Here is my core article on the best uses of American Express Membership Rewards points.

Here is a summary of my valuations:

0.75p – 1.5p per point (estimate, 1:1 ratio) – airline miles

1p per point (estimate, 1:3 ratio) – Radisson Rewards hotel transfers

0.75p per point (estimate, 2:3 ratio) – Marriott Bonvoy hotel transfers

0.66p per point (estimate, 1:2 ratio) – Hilton Honors hotel transfers

0.66p per point (estimate, 15:1 ratio) – Club Eurostar points transfers

0.5p per point (guaranteed, pseudo-cash) – retailer gift cards

0.5p per point (guaranteed, pseudo-cash with potential for upside) – Nectar points

0.45p per point (guaranteed, pseudo-cash) – taking Amazon credit

Read my article on the best Membership Rewards transfers to see how I justify these numbers.

Is Amex really offering 0.9p per point for statement credit?

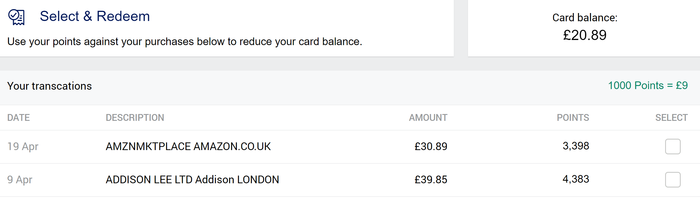

Yes it is. It is NOT advertised yet. However, go to your American Express account and select ‘Use Points for Purchases’ on your Platinum Card home page.

You are taken to a page like this. Select an individual transaction (click to enlarge):

As you can see, I am offered a rate of £9 per 1,000 points.

This deal is NOT available on Business Platinum and Preferred Reward Gold cards unfortunately, or at least not the ones in my house. It only shows on my Platinum card.

Should I redeem my Membership Rewards points for 0.9p each?

That’s not for me to say, of course.

However, as you can see from my numbers above, the bulk of transfers are worth LESS than 0.9p per point.

I would definitely take 0.9p in cash instead of turning my American Express points into Eurostar, Marriott Bonvoy, Radisson Rewards or Hilton Honors points.

This is NOT because these schemes are bad, but because the transfer rate is not generous enough.

(Hilton is currently selling Hilton Honors points with a 100% bonus, which works out at 0.4p each. The link is here, the offer runs to 27th May. Instead of converting Amex points to Hilton Honors at 1:2, it is cheaper to buy Hilton points on your Platinum card and use your Amex points to settle the bill via a statement credit!)

The decision is more marginal for airline miles. Here are the American Express airline transfer partners, all of which are 1:1. If used sensibly, you should get more than 0.9p per airline mile. However, you won’t get SUBSTANTIALLY more than 0.9p per mile and cash in the bank may be more useful to you at the moment.

You should also remember that there are many opportunities throughout the year to buy Avios at around 1p to 1.1p per point. Transferring from Amex at 1:1 into Avios is still a better deal than cashing out for 0.9p, but it is clearly more marginal at this level and the benefit of getting cash in your hand may be high.

My only thought is that, if this offer leads to a reduction in the flow of points to miles, and so a reduction in the money that the airlines are getting from American Express, some airlines may be tempted to offer a generous Membership Rewards transfer bonus to turn the tap back on.

When does this offer end?

It isn’t clear. There are similar offers in France and Canada which are running until 20th July so it MIGHT match that. I imagine that American Express will email everyone in the next day or so.

You can only redeem credit against actual purchases, so your maximum redemption is limited to the value of purchases you make before the closing date.

Amex France and Amex Canada are also offering Platinum cardholders double points on all of their spending for three months. Let’s see if that part of the offer turns up in the UK. If it does, the Platinum card will become the most rewarding card on the market!

PS. If you are not a regular Head for Points visitor, why not sign up for our FREE weekly or daily newsletters? They are full of the latest Avios, airline, hotel and credit card points news and will help you travel better. To join our 70,000 free subscribers, click the button below or visit this page of the site to find out more. Thank you.

Want to earn more points from credit cards? – July 2025 update

If you are looking to apply for a new credit card, here are our top recommendations based on the current sign-up bonuses.

In 2022, Barclaycard launched two exciting new Barclaycard Avios Mastercard cards with a bonus of up to 25,000 Avios. You can apply here.

You qualify for the bonus on these cards even if you have a British Airways American Express card:

Barclaycard Avios Plus Mastercard

Get 25,000 Avios for signing up and an upgrade voucher at £10,000 Read our full review

Barclaycard Avios Mastercard

Get 5,000 Avios for signing up and an upgrade voucher at £20,000 Read our full review

You can see our full directory of all UK cards which earn airline or hotel points here. Here are the best of the other deals currently available.

SPECIAL OFFER: Until 15th July 2025, the sign-up bonus on the Marriott Bonvoy American Express Card is TRIPLED to 60,000 Marriott Bonvoy points. This would convert into 25,000 Avios or into 40 other airline schemes. It would also get you at least £300 of Marriott hotel stays based on our 0.5p per point low-end valuation. Other T&C apply and remain unchanged. Click here for our full card review and click here to apply.

SPECIAL OFFER: Until 14th August 2025, the sign-up bonus on the Hilton Honors Plus debit card is TRIPLED to 30,000 Hilton Honors points. You will also receive Gold Elite status in Hilton Honors for as long as you hold the card. Click here for our full card review and click here to apply.

American Express Preferred Rewards Gold Credit Card

Your best beginner’s card – 20,000 points, FREE for a year & four airport lounge passes Read our full review

British Airways American Express Premium Plus Card

30,000 Avios and the famous annual Companion Voucher voucher Read our full review

The Platinum Card from American Express

50,000 bonus points and great travel benefits – for a large fee Read our full review

Virgin Atlantic Reward+ Mastercard

18,000 bonus points and 1.5 points for every £1 you spend Read our full review

Earning miles and points from small business cards

If you are a sole trader or run a small company, you may also want to check out these offers:

The American Express Business Platinum Card

50,000 points when you sign-up and an annual £200 Amex Travel credit Read our full review

The American Express Business Gold Card

20,000 points sign-up bonus and FREE for a year Read our full review

Capital on Tap Pro Visa

10,500 points (=10,500 Avios) plus good benefits Read our full review

Capital on Tap Visa

NO annual fee, NO FX fees and points worth 0.8 Avios per £1 Read our full review

British Airways American Express Accelerating Business Card

30,000 Avios sign-up bonus – plus annual bonuses of up to 30,000 Avios Read our full review

Freddy

Freddy  Genghis

Genghis  Barry cutters

Barry cutters  AJ

AJ  Chrisasaurus

Chrisasaurus  TGLoyalty

TGLoyalty  Lady London

Lady London  Peter K

Peter K  Rolty

Rolty  S

S  Roltly

Roltly  Bentoni

Bentoni  Rum

Rum  Will

Will  Gary

Gary  Will

Will  No lockdown for moi

No lockdown for moi  Doug M

Doug M  Crafty

Crafty  Waddle

Waddle  Sam

Sam  MinR

MinR

Comments (125)