NEW: Earn 2.5 Avios per £1 when you pay for Qatar Airways tickets via bank transfer

Links on Head for Points may support the site by paying a commission. See here for all partner links.

Qatar Airways has launched an interesting new feature which allows you to earn additional Avios when you pay for a cash ticket via bank transfer.

‘Pay by Bank’ has become increasingly common recently. Merchants love it, of course, because it saves them paying credit card fees.

Consumers hate it because they don’t earn credit card points and (in the UK) lose consumer protection under ‘Section 75’ rules.

The only time I use it is when settling credit card or HMRC bills, when it is more convenient than typing in my debit card details.

What is Qatar Airways offering?

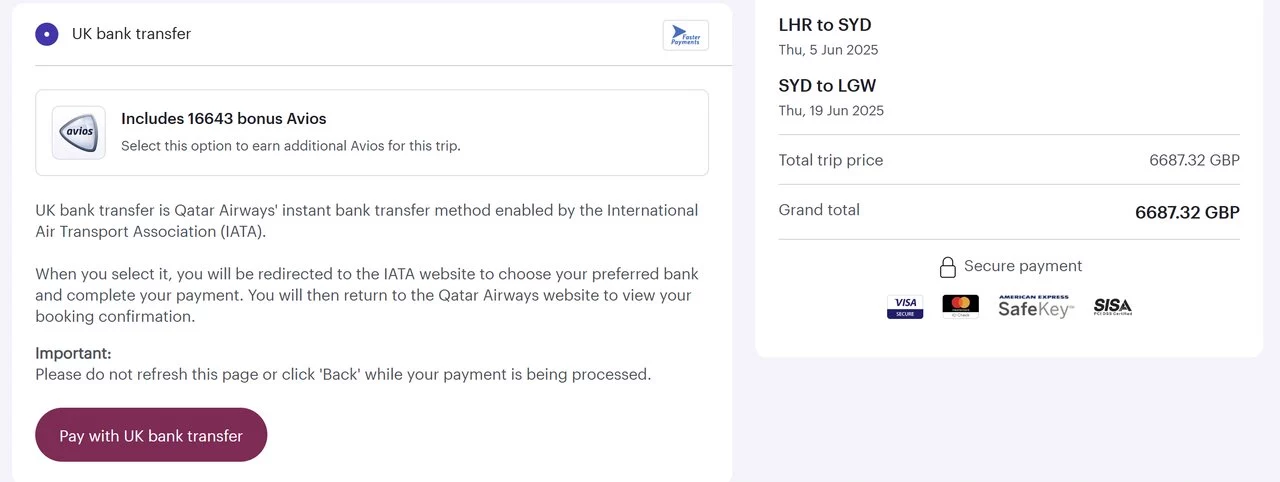

Qatar Airways will give you bonus Avios on your flight if you choose to pay with ‘Pay by Bank’.

Here is an example (click to enlarge):

You will get a bonus 16,643 Avios if you pay £6,687 by bank transfer and not credit card.

This is 2.5 Avios per £1.

Not coincidentally, this is set at a higher level than the Avios you would earn from your credit card. Remember that the headline rates on the key UK airline cards are:

- Virgin Atlantic Reward Mastercard (free) – 0.75 Virgin Points per £1

- Virgin Atlantic Reward+ Mastercard (£160) – 1.5 Avios per £1

- British Airways American Express (free) – 1 Avios per £1

- British Airways American Express Premium Plus (£300) – 1.5 Avios per £1

- Barclaycard Avios Mastercard (free) – 1 Avios per £1

- Barclaycard Avios Plus Mastercard (£240) – 1.5 Avios per £1

The card which comes nearest to 2.5 Avios per £1 is ‘free for a year’ American Express Preferred Rewards Gold. This earns double points (2 per £1) when you spend directly with an airline.

Is Qatar Airways ‘Pay by Bank’ a good deal?

Depending on what credit card you would use otherwise, yes.

The factors to bear in mind are:

- Do you need the credit card spend to get you towards an annual spending voucher or sign-up bonus?

- Are you concerned that you may need to fall back on Section 75 coverage if you have a consumer rights issue with Qatar Airways?

- Do you want to pay immediately? Your credit card would give you a few weeks credit

Yet again (as it did with crediting Avios at check-in, letting you transfer Avios to certain hotel partners and letting you earn and spend Avios virtually everywhere in Hamad Airport) Qatar Airways is trying something innovative with Avios.

If the three points above aren’t an issue, and you are paying in £ so FX fees are not a consideration, taking 2.5 Avios per £1 for using ‘Pay by Bank’ seems attractive.

PS. If you are not a regular Head for Points visitor, why not sign up for our FREE weekly or daily newsletters? They are full of the latest Avios, airline, hotel and credit card points news and will help you travel better. To join our 70,000 free subscribers, click the button below or visit this page of the site to find out more. Thank you.

How to earn Avios from UK credit cards (July 2025)

As a reminder, there are various ways of earning Avios points from UK credit cards. Many cards also have generous sign-up bonuses!

In February 2022, Barclaycard launched two exciting new Barclaycard Avios Mastercard cards with a bonus of up to 25,000 Avios. You can apply here.

You qualify for the bonus on these cards even if you have a British Airways American Express card:

Barclaycard Avios Plus Mastercard

Get 25,000 Avios for signing up and an upgrade voucher at £10,000 Read our full review

Barclaycard Avios Mastercard

Get 5,000 Avios for signing up and an upgrade voucher at £20,000 Read our full review

There are two official British Airways American Express cards with attractive sign-up bonuses:

British Airways American Express Premium Plus Card

30,000 Avios and the famous annual Companion Voucher voucher Read our full review

British Airways American Express Credit Card

5,000 Avios for signing up and an Economy 2-4-1 voucher for spending £15,000 Read our full review

You can also get generous sign-up bonuses by applying for American Express cards which earn Membership Rewards points. These points convert at 1:1 into Avios.

American Express Preferred Rewards Gold Credit Card

Your best beginner’s card – 20,000 points, FREE for a year & four airport lounge passes Read our full review

The Platinum Card from American Express

50,000 bonus points and great travel benefits – for a large fee Read our full review

Run your own business?

We recommend Capital on Tap for limited companies. You earn points worth 0.8 Avios per £1 on the FREE standard card and 1 Avios per £1 on the Pro card. Capital on Tap cards also have no FX fees.

Capital on Tap Visa

NO annual fee, NO FX fees and points worth 0.8 Avios per £1 Read our full review

Capital on Tap Pro Visa

10,500 points (=10,500 Avios) plus good benefits Read our full review

There is also a British Airways American Express card for small businesses:

British Airways American Express Accelerating Business Card

30,000 Avios sign-up bonus – plus annual bonuses of up to 30,000 Avios Read our full review

There are also generous bonuses on the two American Express Business cards, with the points converting at 1:1 into Avios. These cards are open to sole traders as well as limited companies.

The American Express Business Platinum Card

50,000 points when you sign-up and an annual £200 Amex Travel credit Read our full review

The American Express Business Gold Card

20,000 points sign-up bonus and FREE for a year Read our full review

Click here to read our detailed summary of all UK credit cards which earn Avios. This includes both personal and small business cards.

Rick

Rick  Nick

Nick  The real Swiss Tony

The real Swiss Tony  BA Flyer IHG Stayer

BA Flyer IHG Stayer  sayling

sayling  Alex G

Alex G  JDB

JDB  NFH

NFH  Lee D

Lee D  Gabi

Gabi  Lee

Lee  RogerWilco

RogerWilco  Charlie T.

Charlie T.  John

John  Will

Will

Comments (71)